The transaction flow is the same whether you’re using a physical or virtual payment gateway.

Mobile and online payments use digital capture files to package the credit card information rather than output from a credit card reader:

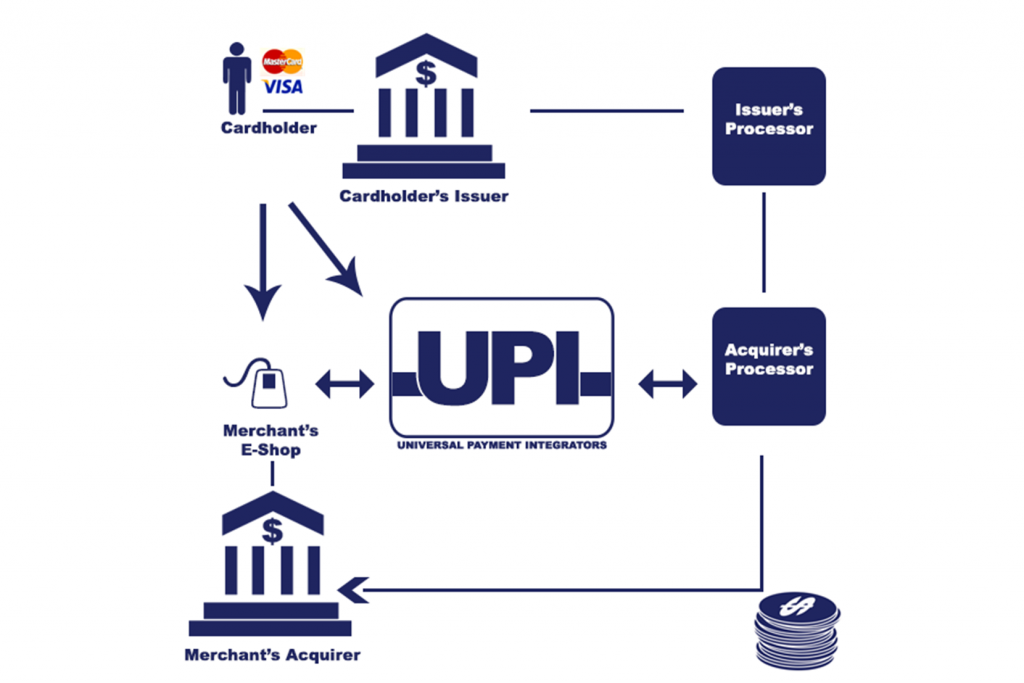

1. The buyer makes a credit card payment through the merchant’s credit card reader or e-commerce site.

2. The payment gateway:

- pushes the transaction information to the acquiring bank (the merchant bank or acquirer);

- determines which credit card network (Visa, MasterCard, Discover, or American Express) issued the buyer’s card;

- routes the transaction information to the correct payment switch

3. The payment switch routes the request to the bank that issued the buyer’s credit card (the issuing bank) and pushes the transaction information onto the correct credit card network.

4. The issuing bank applies fraud detection procedures to determine the legitimacy of the transaction and confirms the buyer has sufficient credit in their account to accommodate the purchase.

5. The issuing bank approves (or rejects) the transaction and sends this information back through the credit card network to the merchant bank and the payment gateway.

Latest News